051: Map Your Money Adventure with Nick True of Mapped Out Money

Nick is a 20-something financial blogger who lives in Chattanooga, TN with his wife Hanna and 3 fur children. His website is MappedOutMoney.com where he focuses on budgeting and helping people learn all of things about money they didn’t learn in school.

Nick is a 20-something financial blogger who lives in Chattanooga, TN with his wife Hanna and 3 fur children. His website is MappedOutMoney.com where he focuses on budgeting and helping people learn all of things about money they didn’t learn in school.

Let’s dig in. Let’s meet today’s Master of Money….

Listen to the Episode with Nick True

Listen to it on iTunes.

Share on Twitter

Map Your Money Adventure with @NickDTrue of Mapped Out Money #mastersofmoney #podcast

Click to tweetThe Difference Between Wants and Really Wants

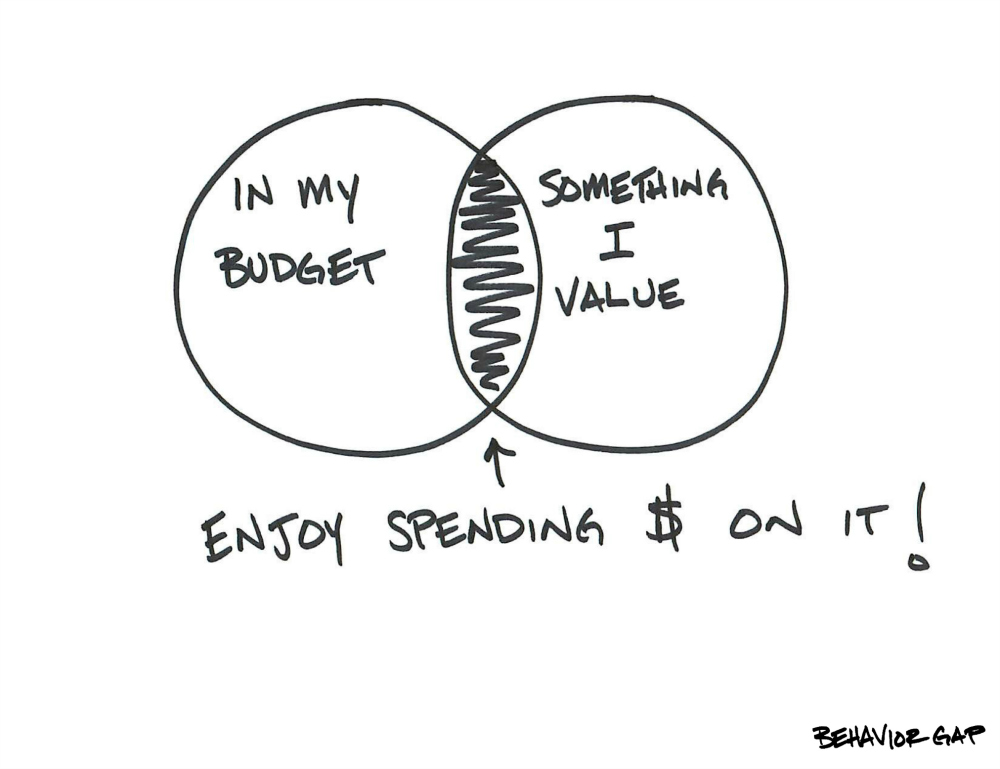

Nick contributes much of his financial success to a simple act – thinking about what he really wants.

Most of us are taught as children the difference between needs and wants. We need food and shelter; we don’t need the candy and the bicycle. Nick sees a further step in the process of deciding needs vs. wants. It’s fine to have a list of things you want but when is the last time you asked yourself what you really want?

Going after the things that he really wants has helped Nick to not fall into the habit of buying anything he wants just because he has the money to do so. Nick’s parents taught him to be disciplined about his spending and the finance books he read as a teen helped him to develop smart money habits.

Nick and his wife have a desire to travel and to get him out of his 9-5 job, so the money decisions they are making now reflect those desires.

Learning to Hustle for What You Want

When Nick was 8 years old, he remembers his dad buying himself a new laptop. And Nick wanted one. He loved playing games on his dad’s computer and he decided to earn enough money to purchase himself a brand new Dell laptop.

It took him two years of selling homemade bread and saving all of his birthday money, along with doing odd jobs, to save the money for his computer. He learned a very important lesson from this experience – that you can work for money if you want something. That money has a definite value.

These lessons continued through Nick’s teen years as he taught piano lessons, sold candy out of a backpack to other students, worked in construction, held a stint at Aeropostale, and had other odd jobs. He was always trying to find ways to make money and then save it.

Credit Cards, College Costs, and Scraping By as a Newlywed

Nick actually went through Dave Ramsey’s Financial Peace University while still in high school and he still thinks it’s a great program. He doesn’t completely agree with Dave’s position on credit cards though.

He got his first credit card while still in college and with a $500 credit limit, he mostly used it to pay for gas. He was very fortunate to get enough scholarship money to completely cover the cost of his college. He also worked part-time throughout college to pay for living expenses with some help from his parents.

Nick and his wife, Hanna, got married when he was a senior in college and she was in her first year of graduate school. Because they were both in college full-time, they lived off of savings and whatever they could make working part-time. This was an extremely stressful time, watching their account balances go down every single month, even though they had planned for it to be this way.

They moved 45 minutes away from the college they were attending to save on rent. They traded Nick’s cool new sports car for a 2001 Honda Civic. They “couponed so hard” that year. They ate Ramen noodles and Hamburger Helper. And they fought.

Hanna had also grown up in a home where money was freely discussed and where she was taught how to save and not go into debt. Nick and Hanna had many money discussions even while they were dating. So what were they fighting about?

Nick admits that most of the problems were his. He has a tendency to stress and freak out a bit when unexpected things happen involving money. When they got married, they knew things were going to be tighter than tight. It wasn’t like one of them was constantly blowing the budget. It was simply difficult watching their balances go down every month and not up.

Spending, Saving, and Investing During the Lean Years

Nick and Hanna got married in June 2014, he graduated the next May, and the first Monday after graduation he started his first “real job.” His degree is in mechanical engineering and when that first direct deposit for his salary went through, Nick felt himself relax a lot.

His starting salary was $64K and that, combined with overtime, allowed him to earn right around $70K that first year. Nick was not only reading personal finance books, he was reading finance blogs as well to keep himself motivated. He’s the first person I’ve met who actually started using Quicken while still in high school to track his savings and spending.

For her part, Hanna was deep in the world of couponing. She attended a conference put on by Southern Savers on how to do grocery store and drugstore deals. Nick was being influenced on spending. The idea was to scrimp and save on things that don’t matter to you and then spend on the things you really want.

Nick opened a ROTH IRA before marriage and was making contributions to it but those years of barely scraping by stopped those contributions. He and Hanna knew that they would need to use his first year’s salary to pay for the 40% of her education that her assistantship wouldn’t cover. And they finally got another car for Nick to replace the Honda Civic that now had over 300K miles on it. Other than that, the only other goal they had for that first year was to contribute the maximum for matching to his company’s 401K.

Managing Emotions Around Finances

Nick is the first to admit that he still has some trouble managing his emotions around financial issues. He has a wealth of knowledge about blogs, books, budgeting, investments, insurance, and other financial products. That emotional side is the one area that he knows he needs to improve on.

This lack of emotional awareness first reared its ugly head on Nick’s and Hanna’s honeymoon, where some unexpected expenses really threw him for a loop. Instead of just rolling with it, he got really upset about it.

They ended up fighting about money quite a bit while on their honeymoon cruise and Nick takes 100% responsibility for it. He let a few hundred dollars come between him and Hanna and let it completely ruin the mood of the trip.

They have found a way to combat this issue by having a budget line item solely dedicated to “unexpected expenses.” However, Nick wants to continue working on this area personally.

No Salary to Big Salary

Because Nick and Hanna lived on so little when they were finishing college, it was quite a shock when Nick got that great job right after graduation. All of a sudden, instead of living on savings and a part-time income, they were living on $70K a year.

The first big change was in their emotions surrounding money. It had been so discouraging to watch their accounts dwindle down each and every month, but now, they were building again. That was a great feeling for both Nick and Hanna.

This new salary also allowed them to have a set amount of money every month for guilt-free spending. You have to remember that before the “big job”, they had zero discretionary money to spend. They began by allowing $70 per month for each of them. While that might sound really small, they were still paying for Hanna’s grad school bills at the time.

They are currently at $45 per month each as they continue to pay those grad school bills and save as much as possible. What can you buy with $45? Well, Nick likes books a whole lot and most recently, he got himself a cool new Gary V t-shirt.

Side Hustling and Credit Card Hacking

Once Nick got his new job, he finally stopped teaching piano. Since that time, he has done a few other things to bring in some side money.

One of the things he’s done is play the credit card game, signing up for several credit cards at once and using the sign-up bonuses and points for things like a new television and a trip. I know a lot of you may be really skeptical about credit card hacking so I asked Nick to explain exactly how he does it.

There’s no way to include all the details in this post so be sure to listen in at 34:51, but the basics are using the credit cards to pay for your monthly recurring expenses and using the sign-up and spending bonuses to add to your income. For example, Nick had a card with a $400 sign-up bonus and a 1% spending bonus for anything over $3K in the first 90 days. That alone is $430 for spending $3K that he would spend anyway on his monthly bills.

It is super important when doing hacks like this to have a serious handle on your spending and remain laser-focused about paying the cards of in full every single month. That’s the only safe way to hack the credit card business. The first time you don’t pay everything in full is when you need to stop.

Using Your Money to Achieve the Things You Really Want

Nick and Hanna love to travel and recently did a ten-day whirlwind trip out West, hitting several sites along the way, including an overnight camping trip at the bottom of the Grand Canyon. Their love for travel, along with Hanna’s upcoming employment, is bringing more travel into their lives.

She will be graduating with a degree in physical therapy and has taken a traveling therapist job. Their most recent purchase as a “really want” has been an Airstream camper and a used truck to pull it with. Her job will place her in a new city every 13 weeks, so when she graduates, Nick will be leaving his job (shhhh, don’t tell his boss), and focusing on his freelance writing work and blogging full-time from the Airstream.

The beauty of this arrangement is that Hanna’s company will give her a housing stipend as part of her salary. They’ll be able to use that to pay campground fees and their living expenses and she will bring in the bulk of their income while Nick continues to build his online business.

Choosing to Take on Debt

In order to purchase the camper and the truck, Nick and Hanna had to take on debt. They plan to pay the truck off as soon as she graduates and they begin traveling by selling Nick’s car and using that cash to pay for the truck. The Airstream has a 72-month loan attached to it which they hope to pay off in 3-4 years.

This lifestyle is a temporary one for them. They would like to do this for the next 5-6 years before settling down to begin a family. Taking on debt for a temporary lifestyle when you’re extremely debt-averse is not an easy decision to make.

One thing that helped Nick come to terms with the decision was doing the math. They’re paying $1200 per month in Chattanooga for rent. The Airstream payment, combined with monthly campground fees, is still less than that. That fact, along with the fact that Airstreams tend to hold their value, helped Nick to see the positive side of hitting the road full-time this fall.

Having all of your finances online is helpful when you want to travel full-time. The main things to consider are getting your mail and making sure your credit card companies know you’re traveling so you aren’t pinged for a stolen card.

Hard Times and Gratitude

When Nick looks back, and at age 23 he doesn’t have very far to look…when he looks back and sees the struggles he and Hanna have faced, the fights, and the lean times, he feels grateful for where they are today.

He has learned the importance of self-awareness around money. He feels strongly that each person needs to figure out their thoughts and beliefs about money. Your budgeting, spending, investing, and saving strategy should be built around those beliefs and personal tendencies.

“It’s been a tough journey, but a great journey, so far and I’m excited about what the future holds.” ~ Nick True

Show Notes

- 00:00Intro

- 01:40 Thinking about what you want vs. what you really want

- 06:10 Nick’s homemade bread business bought his first laptop at age 10

- 12:15 Credit cards, college costs, and scraping by as a newlywed

- 20:10 Spending, saving, and investing during the lean years

- 27:15 Managing emotions around finances

- 31:40 Going from no salary to a big salary

- 34:51 Side hustling and credit card hacking

- 39:50 Living in an Airstream full-time while traveling the U.S.

- 45:00 Choosing to take on debt when you’re debt averse

- 52:00 How the struggles have helped Nick to be grateful

Show Sponsor

Coming soon…

Links/Terms/Concepts from the Show

Full Transcript

Coming soon…

What’s Next?

Have a question? Leave a comment below or use my contact form.

Thanks for listening to this episode. If you like what you hear, please subscribe to the show on iTunes. I want to improve the show, so please leave a rating and review. Tell me what you like and how I could improve.

This show is part of the FinCon Podcast Network and was produced by Steve Stewart.

![How to [Finally] Stick to a Budget](jpg/how-to-finally-stick-to-a-budget.jpg)